5.1 アセット・トークナイゼーションとリアル・ワールド・アセット(RWA)の概念

学習目標 アセット・トークナイゼーションとリアル・ワールド・アセット(RWA)とは何か。

資産デジタル化の進化

資産のトークン化は、資産のデジタル化プロセスにおいて極めて重要な段階である。従来、資産の所有権は紙の書類や集中管理されたデータベースに記録されていた。ブロックチェーン技術の登場により、資産は分散型ネットワーク上でデジタルトークンとして表現され、取引されるようになった。

アセット・トークナイゼーションの定義とプロセス

アセット・トークナイゼーションとは、現実世界に存在する有形・無形の価値ある資産(不動産、美術品、株式、債券、知的財産など)を、ブロックチェーン技術によってデジタルトークンに変換するプロセスを指す。これらのトークンはブロックチェーン上で発行、記録、流通され、原資産の一部または全部の所有権を表します。

実質資産(RWA)

RWAとは、ブロックチェーンの外部に存在し、実際の経済的価値を持つ資産を指す。これらの資産には次のようなものがある:

- 有形資産: 不動産、美術品、収集品、貴金属(金、銀)、自動車、インフラなど。

- 無形資産: 株式、債券、未公開株、貸付金、債権、知的財産(特許、著作権)、炭素クレジット、保険契約など。

RWAのトークン化は、こうしたオフチェーン資産をブロックチェーンのエコシステム(特にDeFi内)に取り込むための重要な橋渡し役となり、流動性を開放して新たな金融機会を創出することを目指す。

5.2 アセット・トークナイゼーションの仕組み

学習目標 現実世界の資産がブロックチェーンを介してデジタルトークンにマッピングされる仕組みを理解する。

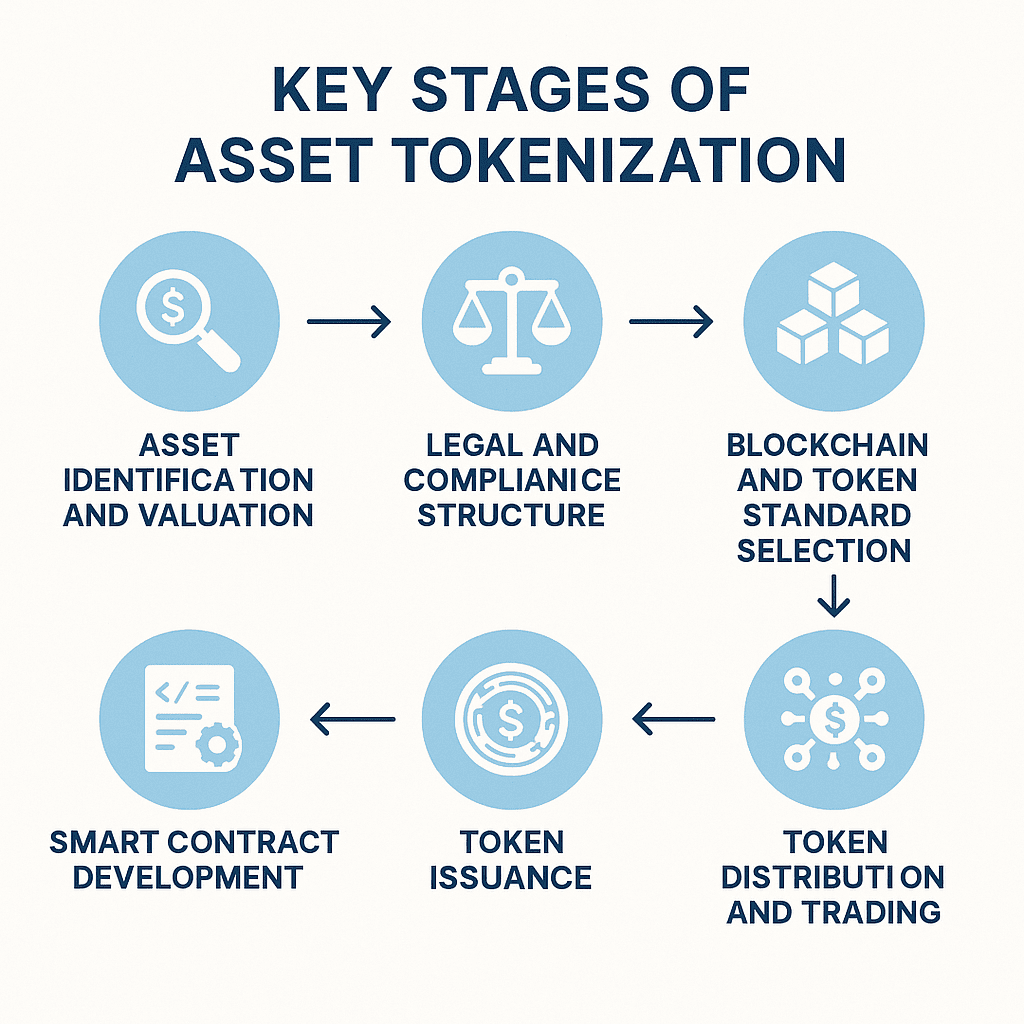

アセット・トークナイゼーションのプロセスには、通常以下のステップが含まれる:

- 資産の選択と評価 トークン化する資産を特定し、価値評価、所有権確認、法的デューデリジェンスを実施する。

- 法的構造の設計: 原資産に関するトークン保有者の法的権利を確保するために、適切な法的枠組みと特別目的会社(SPV)を設立する。これには、信託、ファンド、またはその他の法的構造が関与する可能性がある。

- ブロックチェーンプラットフォームとトークン標準の選択: 適切なブロックチェーン・ネットワーク(Ethereum、Polygon、Solanaなど)とトークン標準(fungibleトークンのERC-20、non-fungibleトークンのERC-721またはERC-1155、または特殊なセキュリティ・トークン標準など)を選択する。

- スマート・コントラクトの開発: スマートコントラクトを作成し、トークンの属性、発行ルール、取引ロジック、権利分配(配当や賃貸収入など)、潜在的なガバナンスメカニズムを定義する。

- 資産の保管と接続: 必要であれば)現実世界の資産を信頼できるカストディ機関に預け、オン・チェーントークンがオフ・チェーン資産の権利と確実にリンク・同期される仕組みを構築する。

- トークンの発行と配布: セキュリティー・トークン・オファリング(STO)またはその他の準拠する方法を通じて、適格な投資家にトークンを発行・配布する。

- セカンダリー・マーケット取引: トークンは準拠した取引所やP2Pプラットフォームで取引でき、流動性を提供する。

トークン化におけるスマート・コントラクトの役割

スマートコントラクトは資産トークン化の中核技術である。所有権の移転、収益の分配、議決権の行使など、資産に関連する条件の実行を自動化し、効率性と透明性を向上させながら手作業の介入を減らすことができる。

フラクショナル・オーナーシップ

トークン化により、高額で不可分の資産(不動産や名画など)をより小さなトークン・シェアに分割することが可能になる。これにより、より多くの小規模投資家が参加できるようになり、投資の敷居が下がる。

5.3 アセット・トークナイゼーションの中核的利点

学習目標 トークン化がいかに資産の流動性とアクセシビリティを高めるかを認識する。

- 資産の流動性の向上: 伝統的に流動性の低い資産(不動産、プライベート・エクイティ、美術品など)をトークン化して小口化することで、グローバルな流通市場での取引が容易になり、流動性が大幅に向上する。

- 投資基準額の引き下げ: フラクショナル・オーナーシップは、小口投資家が高額資産に投資することを可能にし、投資家の裾野を広げ、投資機会を民主化する。

- 24時間365日取引可能 ブロックチェーン・ベースの市場は、従来の取引所の営業時間に妨げられることなく継続的に運営され、取引の柔軟性と効率性を高めることができる。

- 仲介コストの削減と効率性の向上: トークン化とスマートコントラクトは、従来の資産取引における多くの手作業プロセス(清算、決済、所有権登録など)を自動化し、銀行、ブローカー、弁護士への依存を減らし、取引コストと時間を削減することができる。

- 透明性と検証可能性の向上: 所有者の記録と取引履歴は不変のブロックチェーンに記録され、誰でも(許可範囲内で)閲覧・検証できるため、市場の透明性と信頼性が高まる。

- コンポーザビリティの向上: トークン化された資産をDeFiプロトコルに統合することで、トークン化された不動産を担保に融資を行うなど、新たな金融商品やサービスを生み出すことがより容易になる。

- 融資チャネルの拡大: アセット・オーナーに新たな資金調達手段を提供し、より広範なグローバル投資家にアプローチする。

5.4 アセット・トークナイゼーションの主な応用分野

学習目標 さまざまな資産クラスにおけるトークン化の具体的な適用事例を探る。

- 不動産トークン化: 商業用不動産、住宅用不動産、ホテルなどをトークン化することで、投資家は一部の所有権を購入し、賃料収入や上昇分を分け合うことができる。

- 株式と債券のトークン化(セキュリティー・トークン):

- 株だ: 企業の株式をトークン化することで、新興企業の資金調達や既存株式の流通が容易になる。

- 債券: 例えば、フィリピンは国債のトークン化を推進し、発行効率と市場の透明性を高めている。社債もトークン化できる。

- アートとコレクターのトークン化: 名画、骨董品、高級品(時計など)をトークン化することで、投資家は価値の高い収集品を共同で所有したり、アーティストに新たな資金調達や収益化の選択肢を提供したりすることができる。

- 貴金属と商品トークン化: 例えば、(PAXGのように)金をトークン化することで、各トークンが一定量の金の現物所有権を表し、取引や保管を容易にする。

- ファンドの株式トークン化: プライベート・エクイティ、ベンチャー・キャピタル、ヘッジファンドの株式をトークン化することで、その流動性と譲渡性が高まる。

- 知的財産のトークン化: 音楽使用料、特許権、映画権などをトークン化することで、資金調達や収益分配が可能になる。

- 炭素クレジットのトークン化: 炭素排出枠や削減量のトークン化は、炭素市場の流動性と透明性を促進する。

- 債権およびサプライチェーンファイナンス: 企業は売掛債権をトークン化して資金調達し、キャッシュフローを改善することができる。

- 農産物担保ローン: 例えば、スペインのある銀行はブロックチェーンと協力し、農産物(トウモロコシの収穫権など)を信用の担保としてトークン化し、農家の資金需要をサポートしている。

- ステーブルコイン ステーブルコイン自体はRWAトークン化の成功例であり、米ドルのような不換紙幣資産をトークン化し、ブロックチェーン上に持ち込んでいる。

5.5 DeFiにおけるトークン化資産の応用

学習目標 RWAが分散型金融(DeFi)とどのように統合されるかを理解する。

分散型金融(DeFi)にリアルワールドアセット(RWA)を導入することは、ブロックチェーン業界における重要なトレンドであり、伝統的な金融市場と新興のDeFiエコシステムをつなぐことを目的としている。DeFiにおけるRWAの主な用途は以下の通り:

- 貸出の担保としてのRWA:

- DeFiレンディング・プロトコル(MakerDAO、Aave、Compoundなど)は、トークン化されたRWA(トークン化された不動産、国庫証券、債権など)を担保として受け入れ、安定コインやその他の暗号資産を貸し出すことを模索し始めている。

- これにより、DeFiプロトコルで許容される担保の範囲が拡大し、純粋な暗号資産への依存度が低下し、RWA保有者に新たな資金調達チャネルが提供される。

- RWAに基づく利回り商品:

- RWAのキャッシュフロー(家賃やローン利息など)に基づく仕組商品や利回り付きトークンを作成することで、DeFi投資家は暗号市場との相関性が低い安定した収入源を得ることができる。

- 例えば、安定したキャッシュフローを生み出すトークン化されたRWA(短期企業ローンのようなもの)をバンドルし、DeFiユーザーが投資できるようにする。

- 伝統的な金融とDeFiをつなぐ:

- RWAのトークン化は、伝統的な金融市場の膨大な流動性と資産クラスをDeFiにもたらすのに役立ち、DeFiに幅広い応用シナリオとより持続可能な成長を提供します。

- 逆に、DeFiの効率性と透明性は、従来のRWA市場に革新をもたらすこともできる。

- RWAが支援するステーブルコイン: 不換紙幣や暗号資産に加え、RWAはステーブルコインの担保としても機能するため、より多様なステーブルコインの選択肢を提供することができる。

- 流動性プールとRWAのマーケット・メイキング: DEXでRWAトークンの流動性プールを作ることで、ユーザーはこれらの資産を取引し、流動性プロバイダーにリターンを生み出すことができる。

しかし、DeFiにおけるRWAの適用には、資産評価、法的権利、カストディ、クリアリングメカニズムの複雑さ、オフチェーン資産とオンチェーントークンの信頼できる接続の確保といった課題もある。

5.6 アセット・トークナイゼーションの課題とリスク

学習目標 トークン化プロセスにおける主な法的、規制的、技術的リスクを特定する。

法的権利と所有権の定義の問題:

- オン・チェーントークンがオフ・チェーンの物理的資産に対する法的所有権や権利を純粋に表していることを保証することは、最大の課題の一つである。司法管轄区域によって、これに関する法的規定はさまざまです。

- トークン保有者の権利(議決権、収益分配権、償還権など)は明確に定義され、法的に保護される必要がある。

- 特にNFTの美術品や現物資産の所有権については、破産の際の資産の扱いに関する法的枠組みが未整備のままである。

グローバルな規制政策の不確実性:

- アセット・トークナイゼーション(特に証券)は、各国の証券法や金融規制の下で厳しい規制の対象となる。現在、世界的に統一された規制基準は存在しない。

- トークンが有価証券にあたるかどうか、KYC/AMLの実施方法、税務上の取り扱いなど、規制機関はまだ模索中だ。FATFやIOSCOのような国際機関はガイドラインの策定を試みているが、実施状況は国によって異なる。

- 規制政策の変更は、既存のトークン化プロジェクトに大きな影響を与える可能性がある。

伝統的な金融システムの障壁と慣性:

- 伝統的な金融機関は新しいテクノロジーを受け入れるのが遅く、トークン化された資産との互換性の問題に直面する可能性がある。

- 高いコンプライアンス・コストと確立された市場構造が、トークン化の推進を妨げる可能性がある。

スマートコントラクトの脆弱性とプラットフォームのリスク:

- トークン化された資産の発行と管理に使用されるスマートコントラクトには、ハッカーが悪用する可能性のあるプログラミングの脆弱性が含まれている可能性があり、資産の損失につながる。

- トークン発行プラットフォーム、取引所、カストディアンのセキュリティも極めて重要である。

資産評価と価格決定における複雑性:

- アートワークやプライベート・エクイティのような)ユニークなRWAを正確に評価し、流通市場で公正な価格を形成することは難しい。

流動性の問題:

- トークン化は流動性を向上させることを目的としているが、市場参加者が不十分であったり、トークンの設計が貧弱であったりすると、トークン化された資産によっては実際の流動性が限られたものになる可能性がある。

DeFiエコシステム内での内在的リスクの伝達:

- RWAがDeFiプロトコルに統合された場合、プロトコルの脆弱性、ハッキング攻撃、ガバナンスの失敗など、DeFi固有のリスクの影響を受ける可能性もある。

運用の複雑さとユーザー教育:

- 一般の投資家にとって、アセット・トークナイゼーションを理解し参加することは、まだ一定の障壁があるかもしれない。

5.7 アセット・トークナイゼーションの開発動向と市場展望

学習目標 市場予測、機関投資家の参加、将来の発展の方向性を理解する。

巨大な市場の可能性:

- 現在のRWAトークン化市場はまだ初期段階にあるが(評価額は数十億ドル)、多くの研究機関や業界の専門家は、将来的に大きな成長の可能性があると予測している。例えば、ボストン・コンサルティング・グループ(BCG)は、2030年までにトークン化された資産市場は$16兆ドルに達する可能性があると見積もっており、ブロックチェーン業界における最も重要な成長エンジンの一つとなっている。

伝統的金融機関の積極的関与:

- ウォール街の大手企業や大手金融機関(ブラックロック、JPモルガン、シティグループ、ゴールドマン・サックス、フランクリン・テンプルトンなど)は、RWAのトークン化を積極的に模索したり、参加し始めている。彼らは、トークン化されたファンド商品を発売したり、RWA取引プラットフォームを構築したり、関連するテクノロジー企業に投資したりして、ブロックチェーン技術を活用して効率を高めながら、伝統的な金融資産や流動性をブロックチェーン上に取り込むかもしれない。

法的・規制的枠組みの漸進的改善:

- 市場の発展と機関投資家の参加に伴い、規制当局はRWAトークン化市場を規制し、投資家の権利を保護し、イノベーションを促進するため、より明確な法的・規制的枠組みの策定を加速させている。短期的には不確実性が残るものの、長期的な傾向としては、より明確で友好的な規制環境が整いつつある。

絶え間ない技術の進歩:

- ブロックチェーン技術のスケーラビリティ、セキュリティ、相互運用性は絶えず向上している。

- スマート・コントラクトはより強力になり、標準化されつつある。

- オラクル、分散型ID(DID)、プライバシー保護技術などのサポート基盤も発展しており、RWAトークン化をより良くサポートする。

適用シナリオの拡大と深化:

- RWAトークン化の将来的な応用範囲は、債券やファンドといった現在の金融資産から、より広範な現物資産や無形資産へと徐々に広がっていくだろう。さらに、RWAとDeFiの統合は深まり、より革新的な金融商品やサービスが生まれるだろう。

標準化と相互運用性の向上:

- 業界は、より統一されたトークン基準、法的合意、運用プロセスを徐々に形成し、異なるプラットフォームや管轄区域をまたがるRWAの相互運用性を促進していくだろう。

Web3テクノロジーの役割:

- プログラマブルマネー、スマートコントラクト、DAOといったWeb3の中核技術は、決済、融資、資金管理、サプライチェーンファイナンスなど、アセット・トークナイゼーションの多様な応用をさらに推進するだろう。

要約すると、アセット・トークナイゼーションは、伝統的な金融とデジタル・アセットの世界をつなぐ重要な架け橋であり、世界の資本市場の運営を再構築する態勢が整っていると考えられている。課題に直面しているものの、その大きな可能性と積極的な機関投資家の参加は、チャンスに満ちた未来を示唆している。